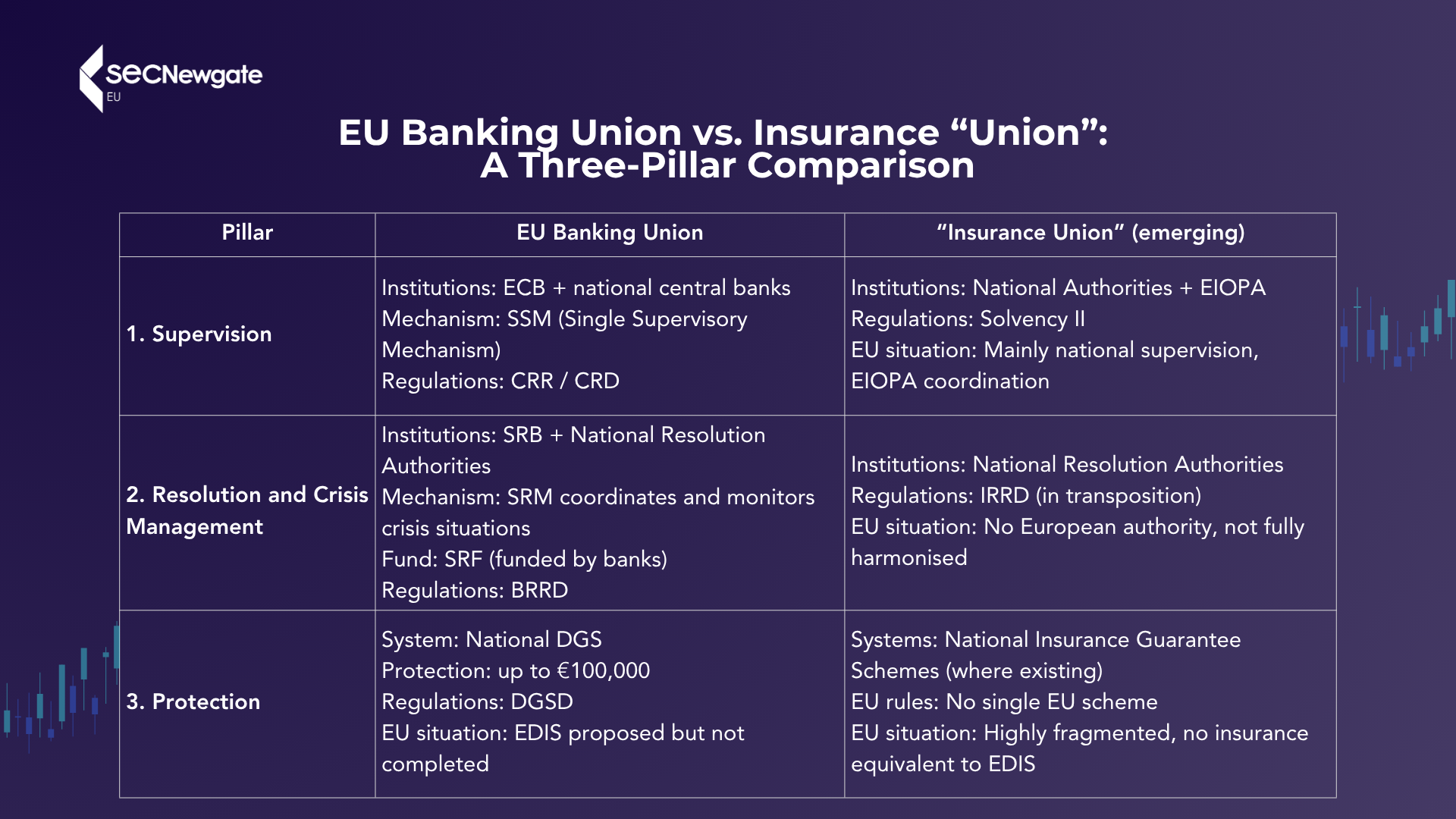

EIOPA, the EU’s insurance regulator, is currently consulting on common minimum standards for Insurance Guarantee Schemes (IGS), essentially, safety nets that protect customers if an insurance company fails. On its own, this might look like a routine regulatory exercise. But viewed alongside two other recent EU initiatives, the updated Solvency II rules and the new Insurance Recovery and Resolution Directive (IRRD), a bigger picture emerges. The EU appears to be gradually building a more unified system for protecting insurance customers, something that could amount to an informal “Insurance Union” that echoes what already exists in the banking sector.

Right now, the level of protection available to insurance customers varies enormously across Europe. Some countries have well-funded guarantee schemes that are ready to step in if an insurer fails. Others have simpler arrangements, or, in some cases, no proper scheme at all. This creates an uneven playing field: insurance products can be sold across EU borders, but the protection a customer actually receives still depends largely on which country they are in. EIOPA’s consultation aims to address this gap by proposing minimum standards for the level of protection customers should receive, how schemes should be funded and governed, and how they should operate across borders.

The real significance of EIOPA’s consultation becomes clear when viewed alongside other regulatory changes. The revised Solvency II rules set standards for how much capital insurers must hold to remain financially sound (prevention). The IRRD creates a framework for winding down failing insurers in an orderly way (resolution). And harmonised Insurance Guarantee Schemes would provide a safety net for customers in the event of a failure (compensation). Together, these three layers form an increasingly joined-up European system for managing insurance risk. The pattern mirrors what happened in banking, where the EU gradually aligned national rules with common European standards, creating the Banking Union. Although the institutional design differs, the underlying approach is similar: steadily replacing a patchwork of national regimes with a more coordinated European framework.

One important question is who pays for all of this. The Banking Union experience shows that introducing common protection mechanisms can strengthen overall financial stability and boost confidence in the single market. But it can also shift costs between countries and between companies. A more harmonised system of Insurance Guarantee Schemes could mean more consistent protection for customers across Europe. Still, it could also create new imbalances. For example, insurers in some countries might face higher funding obligations or compliance costs than others. Over time, these differences could affect how insurers price their products and where they choose to invest. In other words, harmonisation does not necessarily eliminate unevenness; it can simply move it around in less obvious ways.

At the heart of this debate is a fundamental question: who ultimately bears the cost of keeping the insurance sector safe? Solvency II focuses on preventing failures. The IRRD deals with managing them when they occur. Insurance Guarantee Schemes protect customers after the event. Together, they create a multi-layered safety system. But where does the financial burden fall: on insurance companies, on customers through higher premiums, or on national governments? The answer will depend on how these mechanisms are designed, and it will shape not only financial stability but also competition across the European insurance market.

The EIOPA consultation, therefore, matters far beyond its technical detail. It is part of a broader and accelerating shift in how the European insurance sector is regulated. Rules are no longer just about keeping individual insurers financially sound; they are increasingly shaping the market’s structure, including who competes where and on what terms. For the industry, regulation has become a strategic issue with real consequences for business models, pricing, and decisions about expanding into other EU markets.

SEC Newgate helps insurers and financial services organisations navigate this increasingly complex regulatory landscape. This includes tracking and interpreting emerging policy developments from EIOPA, the European Commission, and other EU institutions; spotting early signs of regulatory convergence and assessing their implications for competitiveness and market positioning; supporting participation in consultations; and turning regulatory trends into practical strategic scenarios for decision-makers.

In short, the EIOPA consultation on Insurance Guarantee Schemes is about much more than technical alignment. It is part of a broader shift that is gradually reshaping how insurance risk is managed and how customers are protected across Europe. Whether or not this ever becomes a formal “Insurance Union”, the direction is clear: EU insurance regulation is moving towards deeper integration. For those in the industry, the challenge is not just to respond to regulatory change as it arrives, but to anticipate and help shape it while the rules are still being written.